The conceptual framework of GST

Dr. Akhedan Charan

Additional Commissioner of State Tax

The implementation of GST is a critical milestone in the annals of indirect tax reform. Subsuming numerous union and state taxes, it has transformed them into a single tax. The new tax is being imposed simultaneously by the union and states on the supply of goods and services, with the exception of exempted goods and services, goods that are outside the domain of GST, and transactions that are less than the threshold limits. Previously, it was assessed on the production of goods, the sale of goods, and the provision of services. The introduction of GST was anticipated to provide respite to trade, industry, and consumers by providing a more comprehensive and expansive coverage of input credit. The hashtag ‘GST for new India’ was used by Prime Minister Modi to tweet. ‘The GST had given growth, simplicity, and transparency,’ he wrote. It had improved productivity, intensified formalization, and facilitated the business process.[1] It is imperative that we comprehend the framework of the new tax regime, as GST is a novel taxation system. We will examine the GST framework.

GST Model

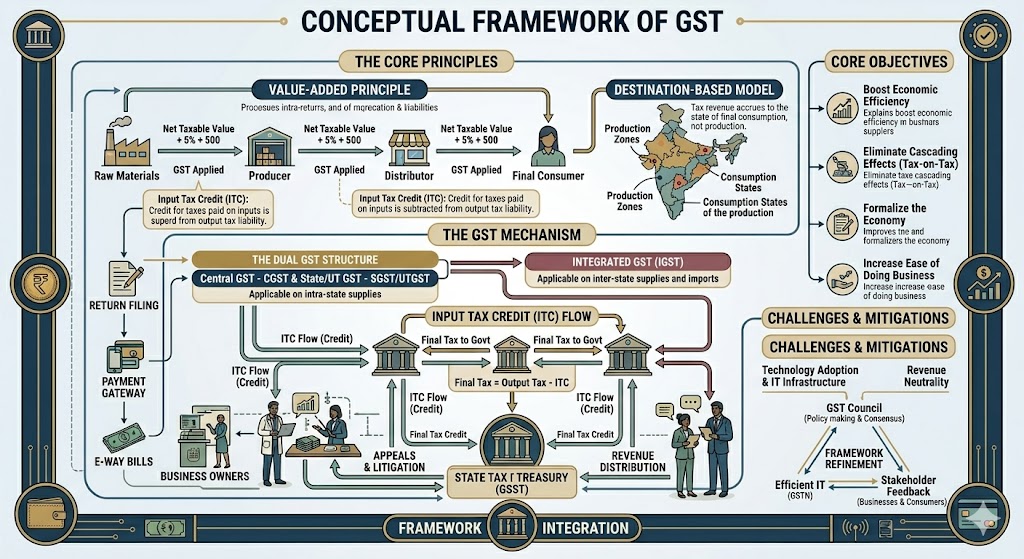

Due to the federal structure of our Constitution, we have elected to implement a dual GST model. The GST imposed by the union is referred to as CGST, while the GST imposed by the state administrations is referred to as SGST. In union territories that lack a legislature, SGST is also referred to as UTGST. The interstate supply of products and services is subject to IGST. IGST is being imposed on the interstate supply of products and services, as well as stock transfers from one state to another. The importation of products and services is considered an interstate supply and is subject to IGST in addition to any applicable customs duties. IGST will be imposed on all imports in the territory of India in accordance with Clause (1) of Article 269A of the Constitution.

IGST is equivalent to CGST and SGST for all interstate supplies of products and services. IGST is levied and collected by the union government, and it is allocated between the union and states in accordance with the method established by Parliament by law, as per the recommendation of the GST Council.

Figures 14.1 and 14.2 depict the working of the GST model. Table 14.1 tells us what payment has to be made under GST.

Figure 14.1 Working of the Dual GST Model within a State

Threshold Limit

The tax threshold is the specific level of revenue at which individuals become liable to pay taxes. Both CGST and SGST are subject to a commonly imposed threshold restriction. Initially, according to the Goods and Services Tax (GST) regulations, individuals or businesses with an annual turnover of less than 20 lakh are exempt from paying taxes. The maximum threshold has been established at 10 lakhs specifically for the special category of North-Eastern and hilly states. The following states are Assam, Arunachal Pradesh, Himachal Pradesh, Uttarakhand, Manipur, Jammu and Kashmir, Mizoram, Meghalaya, Sikkim, Nagaland, and Tripura. However, the Goods and Services Tax (GST) is applicable to the supply of goods and services between different states, regardless of any minimum threshold.[2]

Currently, Companies with a yearly turnover of more than Rs. 40 lakhs (for goods) and Rs. 20 lakhs (for services) must register for GST and pay taxes on their taxable products and services. Businesses having a yearly revenue of less than Rs. 40 lakh are not required to register for GST, but can do so voluntarily. This is useful to businesses since it allows them to claim input tax credits and other perks.

It should be noted that the minimum GST registration turnover limit in India varies by special category state. The special category states have a GST registration threshold limit of Rs. 20 lakhs (for commodities) and Rs. 10 lakhs (for services). These special category states are Arunachal Pradesh, Manipur, Meghalaya, Mizoram, Nagaland, Tripura, and Sikkim.

The GST Council has also advised that all enterprises with a turnover of more than Rs. 40 lakhs register for GST, regardless of their current condition of registration. This level is referred to as ‘turnover for GST registration’.

The minimum GST registration limit in India in 2023 is anticipated to stay at Rs. 40 lakhs. This is likely to bring some assistance to small firms, allowing them to reap the benefits of GST. It is also expected to allow the government to collect taxes from any business, regardless of size.

Source: https://www.indiafilings.com/learn/what-is-the-minimum-turnover-for-gst/

Registration

Business entities that have been officially registered under the GST Act are obligated to remit the Goods and Services Tax (GST). Individuals whose annual sales surpasses 20 lakhs[3] or 10 lakhs[4] in the case of the North-Eastern states, are required to register themselves under GST. The registration for the Goods and Services Tax (GST) is specific to each state and is based on the Permanent Account Number (PAN). Business entities are required to finalize their registration process on the online platform provided by the GSTN portal. Suppliers of goods or services in several states must individually register themselves in each state or Union Territory (UT) where their supply has an impact. An application for registration must be accompanied by a scanned copy of all necessary papers. Upon reviewing the application and scanned documents, the relevant authorities provide a GST registration certificate. In addition, the applicant is assigned a 15-digit GST identity number. Businesses that operate in numerous states and make taxable supplies of goods or services must get separate state-wise registrations.However, if an organization has multiple divisions within a certain state, it is only required to have a single registration. The document must clearly state the main location of the business and any additional locations that function as branches. According to Section 2(18) of the CGST Act, 2017, a business entity that operates multiple business verticals in one state can obtain separate registration for each of these verticals. Under the previous tax system, there were 6.6 million registrations, however under the GST system, the number has climbed to 12 million. There has been a 40 percent rise in the number of individuals who pay taxes. [5]

Revenue Neutral Rate

Revenue Neutral Rate refers to a tax rate that is designed to generate the same amount of revenue as the previous tax rate, without increasing or decreasing the overall tax burden.

The RNR is a tax rate that guarantees that the amount of revenue collected by the new tax system is equal to the amount collected under the prior tax system. Revenue Neutral Rate offsets the negative impact on the revenue of both the central government and state governments resulting from a change in the tax rate. The tax rates have been formulated based on the RNR.

The Government of India (GoI) established a committee led by Arvind Subramanian, who was the Chief Economic Advisor of the Ministry of Finance at the time, to propose the Revenue Neutral Rate (RNR). The committee, headed by Subramanian, proposed a Revenue Neutral Rate of 15-15.5 per cent for the combined taxation of the central government and the state governments. The recommendation is to apply a reduced rate of 12 percent on specific commodities consumed by the poor, and a higher rate of 40 percent on pan masala, tobacco, aerated beverages, and luxury cars due to their negative impact or demerit. The Thirteenth Finance Commission also focused on the Revenue Neutral Rate. The commission calculated and established the RNR at 11 percent. They divided the 11 percent RNR into two rates, 5 percent for CGST and 12 percent for SGST.

The task team, headed by Kelkar, recommended a combined tax rate of 20 percent for both the central and state governments in its report. Out of the total, 20 percent would be allocated, with 12 percent going to the central government and 8 percent to the state governments. A study conducted by Satya Poddar and Amaresh Bagchi proposed that the RNR for both the central government and the state governments should not exceed 12 percent.[6] The rate should be applicable to all products and services, excluding fuels.

Tax rates

The government implemented a five-tier rate system of 0, 5, 12, 18, and 28 percent for the Goods and Services Tax (GST), as shown in Table 14.2. In addition to the five slabs, two additional rates of 3 percent and 0.25 percent were also established. A 3 percent tax levy is applied to precious metals. In addition, the government has chosen to impose a tax rate of 0.25 percent on valuable gemstones and diamonds. In addition, a compensating cess is being imposed on demerit items at a rate higher than the standard 28 percent. The goal of imposing the cess was to provide compensation to the states for the decline in revenue resulting from the alteration in the tax system. The government has classified all commodities into different tax brackets. Therefore, the government has implemented a pricing structure consisting of seven slabs for products and five slabs for services.

Table 14.2 Tax Rate of GST

Source: GST council, as on 24 September, 2018

The Settlement of Accounts

The division of revenue between the central government and the states is what is meant by the term “settlement of account.” This is something that the government does on a somewhat regular basis. The main objective is to settle the account in order to guarantee that the credit of SGST that was used for the payment of IGST is transferred to the center by the state that is exporting the goods. Similarly, the credit for the Integrated Goods and Services Tax (IGST) is utilized for the payment of the State Goods and Services Tax (SGST) by the central government, which transfers the credit to the state that is responsible for importing the goods. After that, the amount of the SGST share in the IGST that was collected on the delivery of B2C is then transferred to the respective states by the respective central government. This means that every single transfer is carried out on the basis of the information that is included in the returns that the taxpayers have submitted.

Format of the Composition

The Goods and Services Tax (GST) includes a provision that is both optional and simpler for small taxpayers. It is not possible for the service provider to participate in this plan. Traders who have an annual total turnover of less than one crore are eligible to participate in the composition scheme.[7] There is a restriction of ₹75 lakh for dealers in Himachal Pradesh and the states that are located in the North-Eastern region. In accordance with this plan, a trader is permitted to pay tax as a predetermined percentage of his turnover without receiving an ITC benefit throughout the year. For the purpose of calculating turnover, PAN is taken into consideration. Table 14.3 provides an overview of the tax rate that applies to the composition system.

Table 14.3 Composition Threshold Limit

Source. Borpuzari. ‘GST: Composition Scheme for Small Taxpayers Extended to ₹1.5 Crore

Administrative Control

At the 21st meeting of the GST Council, which took place on September 9, 2017, the topic of administrative and dual control over assesses was considered. It was during this meeting that the GST Council established the parameters for the administrative control that is exercised on taxpayers. As a consequence of this, the council issued a notification on September 20, 2017, which divided the taxpayers’ base between the central government entity and the states. On the basis of stratified random sampling at the state level, the division is going to be carried out in each state by means of automated computer systems. According to the announcement, the division of control could take into consideration factors such as the geographical location of taxpayers and the sorts of taxpayers. There would be very few exceptions to the rule that the control power under IGST would be cross-powered on the same standard as in CGST and SGST. The ability to collect GST in territorial seas is bestowed upon the states. In Table 14.4, you can see the administrative controls that are associated with the single interface.

If the turnover of the assesses is taken into consideration, then the administrative control will be distributed accordingly. Additionally, the GST Council has broadened the definition of turnover in order to accomplish this goal. When it comes to calculating turnover, the formula will be as given in Table 14.5.

Table 14.4 Administrative Control

source: Indirect tax reform in India, Yashwant Sinha, V.Shrivasatav

Table 14.5 Computation of Turnover

Source: Indirect tax reform in India, Yashwant Sinha, V.Shrivasatav

Compensation to States

As part of the Goods and Services Tax (Compensation to States) Act, there is a clause that provides compensation to the states. As a result of the implementation of the Goods and Services Tax (GST), the legislation provides states with recommendations for compensation for revenue loss. Over the course of a period of five years, the center is planning to reimburse the states. During the transition phase, the base year for determining pay is the fiscal year 2015-2016. The anticipated rate of revenue growth that will be absorbed by a state is going to be fourteen percent. For the purpose of financing the compensation to the states, the central government has imposed a GST compensation cess.[8] Nevertheless, it is important to point out that even this has now ran into complications, as the central government has refrained from paying the compensation that is owed to the states.

Input Tax Credit

When a businessperson is paying tax on the output of products or services, they are eligible for input tax credit (ITC), which allows them to lower the amount of tax that they have previously paid on inputs. The only sum that they are needed to pay is the remaining balance. The cascading effect of taxes can be avoided through the use of this approach. Tax on tax is what is meant by “cascading.” Businesses that are registered under the GST are eligible to claim an input tax credit for the tax that they have paid on the transfer of products or services into their country, or both. With regard to Table 14.6, ITC can be utilized. Tax credit of CGST paid on inputs can only be used for the payment of CGST, and tax credit of SGST/UTGST paid on inputs can only be used for the payment of SGST/UTGST. Both of these tax credits are limited to the payment of CGST. The Indian Goods and Services Tax (CGST) tax credit cannot be utilized to pay the SGST or UTGST, and vice versa.

Table 14.6 Input Tax Credit Uses

Source: Indirect tax reform in India, Yashwant Sinha, V.Shrivasatav

The Accumulation of ITC

The receipt of input tax credit (ITC) occurs when the amount of tax paid on inputs exceeds the amount of tax liability. It is possible to carry it forward to the subsequent fiscal years on the condition that the taxpayer uses it up completely for the payment of their outward tax liability. According to the legislation, there are only two circumstances under which business concerns are eligible to receive a refund of unused ITC: (a) the accumulated credit is due to zero-rated supply, and (b) the inverted duty structure, with a few exceptions. At the conclusion of any given tax period, a registered firm has the ability to get a refund of any unused ITC.

E- Way Bill

It is an electronic document that is provided by a transporter and contains information and instructions that are associated with the transfer of a consignment from one location to another. Along with the names of the consignee and the consignor, the document also specifies the origin point of the shipment, the destination, and the route. It went into effect on April 1, 2018, and it was implemented for all interstate movement of products. States were given the option to choose a date for intrastate supply on or before June 3, 2018, and it was implemented. When it comes to supplies within the state, each and every state has informed it. NCT Delhi was the final state to implement it, going back to the 16th of June in 2018. It is a number that is created electronically and is used to trace the transportation of products on trucks. Every shipment that is worth ₹50,000 or more is required to have an electronic way bill in order to be transported across states. Those transporters who have a consignment value that is less than ₹50,000 are exempt from having to comply with this requirement.

It is possible to purchase an e-way bill for a predetermined number of days, which is determined by the distance that the products need to be transported. In the event that items are to be carried up to 100 kilometers, it is valid for one day. After that, the validity extends by one day for every hundred kilometers that passes. The validity of an e-way bill can be increased online on the transporter’s own system, eliminating the need for the transporter to contact the tax authorities.

E-way Bill Threshold Limit for Different Indian States[9]

The consignment value threshold for the requirement of the e-way bill during interstate transport of goods is only Rs. 50,000. However, multiple states have applied their separate state-specific e-waybill limit with certain particulars to allow intra-state transportation of goods. The details related to e-way threshold limits for different states in the tabulated form are here-

| Indian States | Particulars | E-way Bill Threshold Limit |

| Andhra Pradesh | For all types of taxable goods For transportation of goods, whose value is more than Rs. 50,000 | Rs. 50,000 |

| Arunachal Pradesh | For all types of taxable goods | Rs. 50,000 |

| Assam | For all types of taxable goods | Rs. 50,000 |

| Bihar | For transportation of both taxable and non-taxable goods | More than Rs. 1,00,000 |

| Chhattisgarh | For only a few specific goods | Rs. 50,000 |

| Delhi | For transportation of both taxable and non-taxable goods | Rs. 1,00,000 |

| Goa | Only for specific 22 goods | Rs. 50,000 |

| Gujarat | Not applicable to transport any goods excluding specified goods category for job | No e-way bill |

| Haryana | For all types of taxable goods | Rs. 50,000 |

| Himachal Pradesh | For all types of taxable goods | Rs. 50,000 |

| Jammu and Kashmir | Not applicable for transporting goods within the Jammu and Kashmir Union Territory | No e-way bill |

| Jharkhand | For all goods excluding the specified ones | More than Rs. 1,00,000 |

| Karnataka | For all types of taxable goods | Rs. 50,000 |

| Kerala | For all types of taxable goods | Rs. 50,000 |

| Madhya Pradesh | For specified 11 goods | Rs. 1,00,000 |

| Maharashtra | For all types of taxable goods | Rs. 1,00,000 |

| Manipur | For all types of taxable goods | Rs. 50,000 |

| Meghalaya | For all types of taxable goods | Rs. 50,000 |

| Mizoram | For all types of taxable goods | Rs. 50,000 |

| Nagaland | For all types of taxable goods | Rs. 50,000 |

| Odisha | For all types of taxable goods | Rs. 50,000 |

| Puducherry | For all types of taxable goods | Rs. 50,000 |

| Punjab | For all types of taxable goods | Rs. 1,00,000 |

| Rajasthan | For every taxable good other than the ones categorized under Chapter 24 | Between Rs. 50,000 and Rs. 1,00,000 |

| Sikkim | For all types of taxable goods | Rs. 50,000 |

| Tamil Nadu | For all types of taxable goods | Rs. 1,00,000 |

| Telangana | For all types of taxable goods | Rs. 50,000 |

| Tripura | For all types of taxable goods | Rs. 50,000 |

| Uttar Pradesh | For all types of taxable goods | Rs. 50,000 |

| Uttarakhand | For all types of taxable goods | Rs. 50,000 |

| West Bengal | For all types of taxable goods | Rs. 1,00,000 |

Terminologies to Learn to Understand E-way Bill for States

You should also learn a few common terminologies for understanding state-wise e-way bill limits. These include the following-

E-way Bill

E-way bill or electronic way bill refers to a document or receipt produced by a reliable carrier who instructs and provides details on the transportation of various goods. These include the origin, the consignee, the consignor, the transporter, the destination, and the rail or vehicle data. Understanding state-wise e-way bill limits is especially essential for every business that is involved in the regular transport of goods.

According to the CGST Rule 138, businesses should submit transport-related information before they commence the transportation of goods. Moreover, the rule is applicable whether the movement is for supplies or purposes excluding the supply.

Format of an E-way Bill

The e-way bill consists of a valid e-way bill number, the date of bill generation, and an individual’s GST number of a transporter. It provides the respective details to the transporter, consignee, and consignor. The e-way bill contains two different parts, which are-

Part A of the GST form EWB-1

Part A contains GST information of the consignee and the recipient, challan or invoice number and its date, pin code of the delivery destination, the reason for transporting the goods, original goods’ value, HSN or harmonized nomenclature code, and transport document number. Here, the transport document number may be anything from your railway receipt number, goods receipt number, lading number bill, or airway bill number.

Part B of the GST form EWB-1

Part B only contains the vehicle number of a vehicle.

Benefits to Learn State-wise E-way Bill Limit

Today, knowing the effects of state-wise e-waybill limits on businesses is essential for many reasons, which are as follows-

Limited Paper Documents

The introduction of state-wise e-way bills has reduced the use of paper documents. Hence, both businesses and government officials may go with an environment-friendly option. Furthermore, businesses may not need to bear the hassle to carrying or safeguarding multiple paper documents.

Reduced Wait Times at Checkpoints

Improved efficiency of the e-way bill has reduced the wait times at different checkpoints. This further leads to improved efficiency in the transportation systems and reduced transport costs.

Reduction in Physical Interaction

Business representatives and transporters are no longer required to visit the checkpoints or offices of different tax authorities to generate transport documents. Instead, businesses only need to focus on the state-specific e-way bill impact on transactions to conduct the entire process online.

Involves Fast and Easy Processes

E-way bill generation for individual states is fast and easy based on a user-friendly interface. Moreover, a simple interface has allowed businesses to know state-based thresholds easily. Hence, the importance of knowing e-way bill thresholds by state further boosts tax compliance among business entities under the entire GST regime.

Latest Amendments/Updates on E-way Bill Thresholds

Updated on 4th August 2021

Blocking of e-way bills because of non-filing GSTR will resume from 15th August 2021.

Updated on 29th August 2021

Taxpayers have obtained relief from blocking their E-way bills of GSTR-1 and GSTR-3B from March 2021 to May 2021.

Updated on 18th May 2021

CBIC or the Central Board of Indirect Taxes clarified that GSTINs blocking to generation of e-way bills apply only to defaulting suppliers. However, the rule does not apply to transporters and recipients.

Updated on 1st June 2021 In this update, the e-way bill portal cleared that any suspended GSTINs will not generate any e-way bill. However, they may be transporters or recipients to generate e-way bills. Furthermore, the amendment will update the transportation mode to Ship/Road cum Ship instead of Ship to achieve flexibility in report

[1] Business Standard, July 2, 2018

[2] “Live Mint” June 30, 2017

[3] GST Council raised the exemption limit from 20 lakh to 40 lakh during its 32nd meeting.

[4] GST Council raised the exemption ceiling to 20 lakh from the previous cap of ₹10 lakh during its 32nd meeting.

[5] Indirect Tax Reform in India, Yashawan Sinha and V. K. Shrivastav

[6] Poddar and Bagchi’s ‘Revenue-Neutral Rate for GST’

[7] During the 23rd meeting of the GST Council, it was recommended that the turnover ceiling be increased to ₹1.5 Cr. Therefore, the necessary amendments in the Act have been carried out

[8] CBIC, “Goods and Service Tax (GST),” pages 29-30

[9] https://www.captainbiz.com/blogs/e-way-bill-generation-limit-state-wise-threshold-and-its-impact-on-businesses/