The GST administration

Dr. Akhedan Charan

Additional Commissioner of State Tax

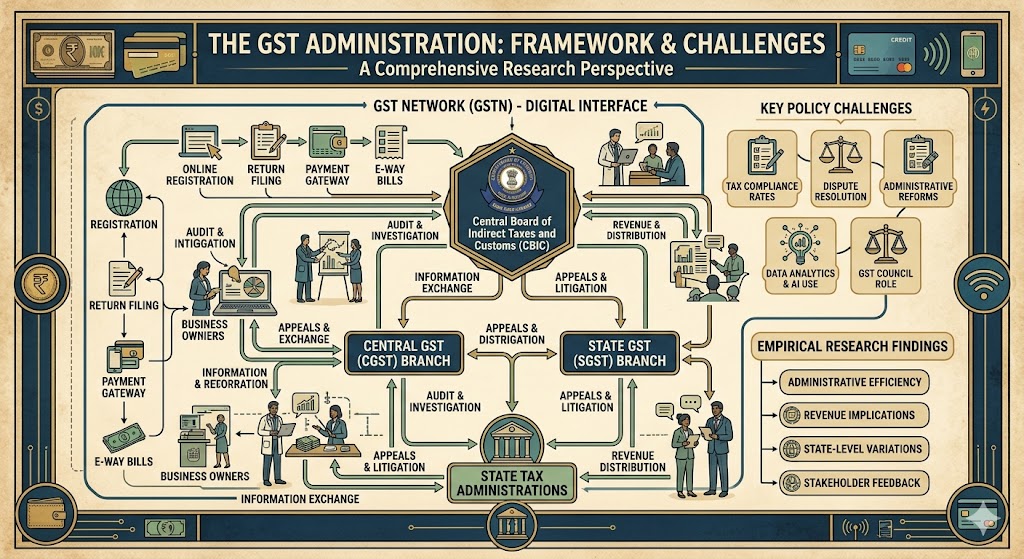

The Central Board of Excise and Customs had the responsibility of overseeing the implementation of the indirect tax system in the country. GST is a form of indirect taxation. The successful execution of the new tax system required the establishment of a new CBIC, the GST Council, and the Appellate Tribunal (AT) and Advance Ruling Authority (ARA) to ensure the efficient operation of the new tax regime. In addition, the GST Network (GSTN) is also playing a crucial part in this entire process. This chapter will focus on the role and duty of various authorities.

The GST Council

The inception of the GST Council can be attributed to Yashwant Sinha, who advocated for the establishment of the Empowered Committee of State Finance Ministers while serving as the finance minister. Subsequently, the EC was tasked with formulating the framework for the implementation of the Goods and Services Tax (GST). There was uncertainty on whether the EC should retain control over the administration of the GST or if a new entity should be established for this purpose. Ultimately, the government made the decision to grant constitutional standing to it by incorporating a provision for the GST Council in Article 279A of the Constitution (101st Amendment) Act of India. The presidential decree issued on September 15, 2016, officially sanctioned the establishment of the GST Council. The Council members comprise representatives from both the union and state governments. The Council has the authority to establish its own method for its operation. The council’s headquarters is located in New Delhi. The Secretary (Revenue) serves as the secretary of the council by virtue of their position. The federal government allocates funding to cover all the expenses of the Council.

Individuals who are part of the council

The GST Council is a collaborative platform that includes both the central government and the state governments. The union representatives in the council possess a voting share of one-third, whereas the states possess a voting share of two-thirds. The council is composed of the following members:

1. Union Finance Minister – Chairperson.

2. Union Minister of State responsible for the departments of Revenue or Finance- Member

3. Minister in charge of finance and taxation

a. Alternatively, any minister designated by state governments can also be a member.

According to Section 12(3) of the Constitution, the members of the GST Council have the authority to select a vice-chairman from their own group for a duration determined by the members. The chairperson of CBIC holds a permanent invitee status, which means they are allowed to attend all council meetings but do not have voting rights. The GST Council has the authority to provide recommendations on the following matters:

1. Taxes, surcharges, and cesses imposed by the central government, state governments, and local organizations that can be included under the framework of the Goods and Services Tax (GST).

2. The threshold limit of turnover refers to the specific amount below which products and services may be exempted from tax.

3. The law related to the modeling of goods and services, the principles of levying taxes, the distribution of Integrated Goods and Services Tax (IGST), and the factors that determine the place of supply.

4. Exemption of goods and services from GST

5. The GST rates, which include a minimum rate as well as a range of rates, are being discussed.

6. Implementing preferential rates during specified time periods to generate extra income in the event of a disaster or natural catastrophe.

7. Specific regulations pertaining to Himachal Pradesh, Jammu & Kashmir, the North-Eastern States, and Uttarakhand.

8. Any other issue as determined by the Council

Functions

The responsibilities of the GST Council are outlined in Section 12(6) of the Constitution. According to this clause, the Council is responsible for ensuring that the structure of GST is standardized and that the national market is unified.

Quorum and Decision of Meeting

According to Section 12(7) of the Constitution, the minimum number of members required for a meeting to proceed is half of the total number of the Council. The Council’s decisions will be made by a majority of at least three-fourths of the weighted votes of the members who are present and voting. Therefore, in order to achieve a majority of three-fourths, it would be necessary to have the support of the central government and at least 20 states. According to Section 12(10) of the Constitution, the actions or proceedings of the Council cannot be deemed illegal for the reasons stated below:

1. Any available position within the Council

2. Any flaw in the process of appointing an individual as a member of the Council

3. Any procedural anomaly of the Council

Resolution of conflicts

If a disagreement occurs, the Council has the authority to create a system to settle it. According to Section 12(11) of the Constitution, the Council is required to establish a process for resolving any disagreements that may occur.

1. In the relationship between the central government and one or more states

2. Between the central government and one or more states on one side, and one or more states on the other side.

3. Amongst multiple states

Meetings

The GST Council convenes periodically to address the technical issues in the recently implemented tax system. A total of 52 council meetings have been conducted thus far. The inaugural conference took place on September 22-23, 2016, while the 52th meeting was convened on October 7th, 2023. The date and location of the meetings are indicated in Table 13.1

Table 13.1 GST Council Meetings

The Goods and Services Tax Network (GSTN)

The structure of GSTN was created by the EC of State Finance Ministers.[1] The government chose NSDL as the technology partner to support the development of the national information utility.[2] In accordance with Section 25 of the Companies Act, 1956, the government established GSTN as a privately held corporation in March 2013.

The authorized capital of GSTN is 10 crore. The government possesses a 49 percent ownership interest that is evenly distributed between the federal government and the state governments. The remaining 51 percent is owned by non-governmental financial institutions.[3] Nevertheless, the GST Council has modified the distribution of ownership in GSTN during its 27th meeting. The Council has granted approval for private/non-governmental institutions to acquire a 51 percent stake in the GSTN, totaling 5.1 crore. This cash would be evenly divided between the central government and the state governments.

GSTN offers three primary services: registration, tax payment, and tax return processing. The objective of GSTN is to offer a standardized platform for taxpayers and facilitate the sharing of infrastructure between the central and state governments. The central and state governments are enrolling taxpayers in the Goods and Services Tax Network (GSTN). As of now, more than 1.22 crore enterprises have been registered under the Goods and Services Tax Network (GSTN). [4]

Central Board of Indirect Tax and Customs

In 1924, the government implemented the Central Board of Revenue Act to oversee the collection of both direct and indirect taxes. Subsequently, in 1963, the government divided the board into the Central Board of Direct Taxes (CBDT) and the Central Board of Excise and Customs (CBEC). In 2018, the CBEC was renamed as the Central Board of Indirect Taxes and Customs (CBIC). It is expected to play a significant role in the implementation of GST. It is a division of the revenue department within the Ministry of Finance of the Government of the country. The primary responsibility of CBIC is to develop policies regarding the imposition and collection of all indirect taxes.

Appellate Tribunal

The Appellate Tribunal (AT) is a legal entity that possesses some characteristics of a judicial body i.e. quasi- judicial body. The second forum will serve as an intermediary in resolving indirect tax disputes between the states and the central government. The tribunal will consider appeals against the order issued by the AT/Revision Tribunal. The provisions for (AT) is outlined in Sections 109-116 of the Central Goods and Services Tax (CGST) Act, 2017. The location will be in Delhi. An individual has the option to approach the First Appellate Authority in order to challenge the ruling made by the Adjudicating Authority.[5] Additionally, this clause has been approved by states in the SGST Act. The government has granted approval for the establishment of the Goods and Services Tax Appellate Tribunal, also referred to as GST AT, on 23 January 2019. The AT would comprise a president and two technical members,[6] with one person assigned to oversee the central Goods and Services Tax (GST) and another member assigned to oversee the state GST. Additionally, each bench of the tribunal would have one judicial member.

Advanced Ruling Authority (ARA)

Since the implementation of GST, the commerce and industrial sectors have encountered several challenges such as difficulties in submitting returns, uncertainty over the creation of e-way bills, and complications in claiming legacy CENVAT credit through the TRAN-1 form, among other issues. In order to address these problems, the GST law includes a provision for the establishment of an Advance Ruling Authority (ARA). States have established ARAs to address taxation issues within their individual jurisdictions. However, it has been observed that the ARAs of different states have issued conflicting rulings on the same matter. Creating such powers becomes futile if their objective is undermined. The Telangana ARA and the West Bengal ARA issued conflicting judgments regarding the approach to be taken in reaching a decision in a matter. In its 31st meeting on 22 December 2018, the GST Council has given its approval for the establishment of a Centralized Appellate Authority for Advance Ruling to address this issue. The establishment of a National ARA will eliminate contradictory judgments issued by the state ARAs. The goal of ARA is to proactively inform taxpayers about the handling of transactions beforehand.

[1] GoI, Union Budget for the fiscal year 2012-13

[2] Gol, Budget Speech, 2011-12

[3] ICICI Bank (10%), NSE SI (10%), HDFC and HSFC Bank (20%), and LIC HF (10%).

[4] Indirect Tax Reform in India, Yashawan Sinha and V. K. Shrivastav

[5] https://www.hrblock.in/earlygst/appeal-first-appellate-authority-gst/.

[6] As per Section 109 of Chapter XVIII of the CGST Act, 2017